Getting The Bankruptcy Victoria To Work

Table of ContentsInsolvency Melbourne Things To Know Before You BuyMore About Bankruptcy Melbourne7 Simple Techniques For Bankruptcy Australia7 Easy Facts About Bankrupt Melbourne DescribedThe 8-Minute Rule for Liquidation Melbourne

Occasionally, where there is no equity in an asset the trustee will certainly enable you to preserve it (for instance where your mortgage is virtually the like, or more then, the worth of your house). Understand that the home might still be offered later if the value goes up and/or the home loan drops.Your home may be taken and also sold by the trustee at any type of time, also after you have actually been released from personal bankruptcy. You might possess residential property with an additional individual such as your partner, de facto partner or one more member of the family. if you declare bankruptcy, the other proprietor(s) will certainly be offered the option to get your share of the property from the trustee in insolvency - Bankruptcy.

Even transactions which occurred longer than 5 years ago can be challenged by the trustee if it can be revealed you were attempting to conceal riches from your lenders. There is no minimum amount of financial obligation needed for you, a debtor, to provide an application for bankruptcy. Yet the Official Receiver can turn down a borrower's petition if it assumes you: Would certainly have the ability to pay the financial debts within an affordable time; and also that either: You hesitate to pay one or every one of his/her debts; or You have actually been previously insolvent on a borrower's request a minimum of 3 times or at the very least as soon as in the past 5 years.

Things about Insolvency Melbourne

Jodhi declared bankruptcy on a $5,000 charge card financial debt. Two years later she inherited $40,000 when her grandfather passed away. By after that the price of annulling the personal bankruptcy (paying financial debt consisting of rate of interest, plus all the costs and also charges of the trustee) was over $30,000, indicating that she got less than $10,000 from her inheritance.

There are offenses associated with bankruptcy for which debtors may be prosecuted. There is additionally an offense associated to gambling or unsafe conjecture, and also an additional for sustaining credit rating which it was clear you could not pay.

If you are concerned regarding any one of these issues, talk with your financial counsellor or obtain lawful suggestions. Take into consideration stating insolvency if: You will certainly not have sufficient money to live on if you make all the regular monthly settlements you are needed to make to your creditors; You do not have assets that can be marketed to pay back the debts (eg you rent your residence and also your only other property is an automobile worth under $8100, as at September 2020); You have actually consulted from a cost-free as well as visit our website independent economic counsellor and checked out various other alternatives; and You understand and can deal with the restrictions that personal bankruptcy will certainly bring currently and also in the future.

Get This Report on Bankruptcy Advice Melbourne

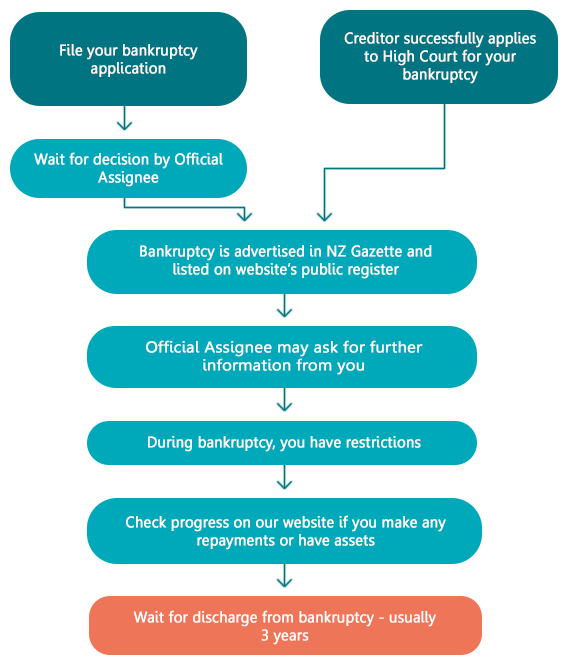

Step 2 Many insolvency applications currently need to be made online. Bankruptcy Australia. See the Australian Financial Safety Authority for basic standards to request personal bankruptcy. Prior to you can proclaim bankruptcy by completing the Personal bankruptcy Kind, be prepared to: Create an account with AFSA before you can begin; Verify your name and contact information; Submit documents that prove your identity.

AFSA will certainly mail the documents to your postal address. Financial counsellors can also aid you. A lot of monetary therapy agencies have accessibility to the paper variation of the Bankruptcy Form. Financial counsellors can aid you to finish the types and advise you on any kind of problems you may be running into regarding the bankruptcy procedure.

Some Of Liquidation Melbourne

List all your possessions also if you might believe the home is protected in insolvency. You need to call the National Debt Hotline on 1800Â 007Â 007 if you need details guidance on any of your financial debts.

Once you're adjudged bankrupt, financial institutions can't continue to chase you for any kind of financial obligation consisted of in your bankruptcy. On discharge from your bankruptcy, you are launched from the majority of the financial obligations included in your go to website personal bankruptcy as well as you do not need to pay any kind of more of the exceptional amount owed to the financial institutions consisted of in your personal bankruptcy.

5 Simple Techniques For Bankruptcy Advice Melbourne

contingent financial debts e. g. when you authorize as guarantor for a friend's financing arrangement. You don't have to pay any type of cash now but you might need to settle the financial debt in the future if your close friend doesn't pay. These debts are included in your personal bankruptcy, however will only be paid from profits if the contingency really emerges - Bankruptcy Victoria.

So while you are launched from the debt on your discharge, the other person is not. overseas financial obligation Any financial debts owed to a financial institution that is based overseas are included in the New Zealand insolvency. Nonetheless, if you go back to the country where the liability was sustained then that creditor is able to recover any of the debt that you still owe because nation.

Safe debt is left out from personal bankruptcies due to the fact that the financial institution can repossess the home if you don't pay, and sell it to get their cash back. If there's still cash owing after they've repossessed and sold the residential or commercial property, that amount becomes an unsecured debt and is after that consisted of in the insolvency.